The Australian Financial Services Licence: What It is, How to Get One & When You Need One

The Australian financial services market is heavily regulated in Australia – and one of the most basic requirements is the need to hold an Australian Financial Services Licence. This is the licence required by entities to conduct a business involving the provision of financial services and products.

Below, we’ll outline what an Australian Financial Service Licence is, who needs one and how you can get one.

What is an Australian Financial Services Licence?

An Australian financial services licence (AFSL) is a licence granted by the Australian Securities & Investments Commission (ASIC) to:

- Provide financial advice

- Deal with a financial product (such as securities)

- Operate a ‘registered scheme’

- Provide services as a traditional trustee company

- Make a market for a financial product (for instance, where you would quote a price to sell or buy financial products like bonds)

Put simply, if you want to operate a financial services business, you’ll need an AFSL.

Who needs an AFSL?

Anybody who wants to run a financial services business will need an AFSL.

Chapter 7 of the Corporations Act 2001 (Cth), the primary corporations legislation in Australia, says that entities must hold an AFSL if they carry on a business involving the provision of a financial service or a financial product.

“Financial services” is a broad term but can include:

- Advising clients on whether to buy or sell a particular financial instrument

- Issuing shares, or arranging for the purchase and sale of stock

- Custodial services

- Depository services

- Crowdfunding services

- Claims handing and settling services

- Superannuation trustee services

A “financial product” is defined as a facility through which a person makes a financial investment, manages financial risk and makes non-cash payments.

Some financial products include (but aren’t limited to):

- Cash

- General insurance

- Foreign exchange

- Securities

- Derivatives

- Carbon units

- Government bonds

- Managed Investment Schemes

- Superannuation

You can apply to provide one or more of the above financial services or products, to retail and/or wholesale clients.

But as you can glean from the above, it’s tricky to properly delineate between financial products and services. This means it’s easy to inaccurately or wrongly define the kind of services you’re providing.

Warning: Penalties apply if you don’t get one

If you operate without an AFSL in circumstances where you need one, or your AFSL doesn’t cover the services you’re providing, you would be guilty of an offence and liable for substantial penalties – including imprisonment.

Section 911A of the Corporations Act says that a person who carries out a financial services business must hold an AFSL covering these services.

Failing to comply with that section is an offence, and you could be liable for:

- a jail term of up to five years

- a fine of up to $133,200 for an individual and $1.33 million for a corporation

Failure to comply is also a civil contravention. This means you could also be liable for

- a civil penalty of up to $1.11 million; or

- three times the benefit obtained / detriment avoided (for an individual) or the greater of $11.1 million, three times the benefit obtained or detriment avoided, or 10% of annual turnover (capped at 2.5 million penalty units) for a body corporate.

In December 2020, ASIC published a statement noting a ‘significant escalation’ in complaints about unlicenced conduct. This included unlicenced advice being provided through seminars, social media and also on websites.

The above case is just one of many of examples where ASIC has leaded investigations into individuals resulting in criminal charges being laid against them.

Exemption from holding an AFSL

Not everybody needs an AFSL in the financial services industry. Some exemptions, broadly stated, include:

- Foreign financial services providers (until 31 March 2023)

- Financial counselling agencies (except for rural financial counselling agencies)

- Foreign collective investment schemes

- Businesses carried on “in connection” with an AFSL licensee

- Business operating financial services under the authority of another regulatory agency (for example, the Australian Prudential Regulatory Authority)

- Circumstances where your financial services business are not the only or main focus of the activity

It is important that you seek professional advice to determine whether you are required from holding an AFSL or not.

Federal Election 2022 uncertainty: changes to AFSL exemptions?

In February 2022, the Federal Government introduced a bill to change current AFSL exemptions under the Corporations Act. This included introducing a ‘professional investor’ and ‘comparable regulator’ exemption to replace certain existing exemptions.

The bill has been tabled in Parliament, but it has not become law yet. It may not become law at all before the Federal Election (which will happen in May 2022).

There is therefore some uncertainty as to whether these changes will come into place – especially if we experience a change in government.

How to get your AFSL

The easiest way to obtain your AFSL is to apply online through ASIC’s eLicensing system. You can work on your application, save it in draft and then resume anytime.

Each application for an AFSL is assessed by ASIC. They will look closely at your application to determine if:

- you are competent enough to carry out the financial service business you’ve specified;

- you have enough financial resources to carry out the business; and

- you can meet the other requirements of a licensee (the required training, insurance, dispute resolution and compliance obligations).

If you can meet these essential criteria, ASIC will grant you an AFSL.

AFSL conditions

There’s getting your AFSL – and then there’s keeping it. As an AFSL holders, you’ll need to:

- Comply with your licence conditions and all financial services legislation

- Take reasonable steps to make sure that your representatives are adequately trained, and also comply with financial services legislation

- Do all things necessary to make sure your financial services are:

- covered by your licence; and

- provided honestly, fairly and efficiently.

- Have adequate arrangements in place to manage conflicts of interest that may arise from time to time

- Maintain the competence to provide financial services (via your ‘Responsible Managers’)

- Have a system of dispute resolution if you provide services to retail clients (includes being a member of an ASC approved external dispute resolution scheme)

- Have adequate resources in place to provide your financial services and their supervision (this includes both technology, human and financial resources)

This is not an exhaustive list of conditions. Entities with an AFSL must ensure that they comply with all the conditions listed in section 912A of the Corporations Act. Failure to do so may in ASIC prosecution, penalties and imprisonment in the worst cases.

Case study: Westpac fined over ‘misleading’ consumer credit insurance in April 2022

ASIC commenced civil proceedings against Westpac in 2021. They alleged that the bank sold consumer credit insurance (CCI) to customers – and charged those customers – even though they had never requested CCI. Hundreds of customers allegedly complained to ASIC that they were debited CCI premiums having never asked for it.

ASIC alleged that each time Westpac did this to a customer, it failed to do all things necessary to ensure that its financial services covered by its AFSL were provided “efficiently, honestly and fairly” and therefore contravened section 912A of the Corporations Act.

In April 2022, the Federal Court fined Westpac $1.5 million, finding that Westpac had issued CCI policies to 141 customers who didn’t request it.

After the Federal Court handed down its decision, ASIC’s Deputy Chair Sarah Court said:

“The industry is now clearly on notice as to the consumer associated with the mis-selling of these products. And under the new penalty regime ASIC will be seeking significantly increased penalties for misconduct of this kind”.

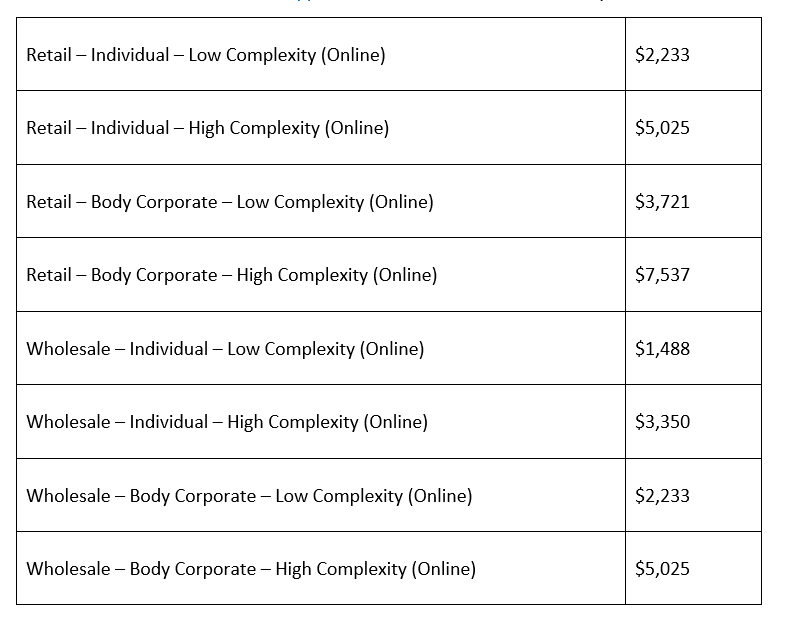

What does an AFSL cost?

Applying for an AFSL can cost between $1,488 to $7,537.

This, however, only includes the initial application fee. Preparing your application may incur legal and compliance costs, accounting costs and other associated costs you may spend to ensure your application is correct.

The total cost can therefore cost anywhere between $10,000 to $60,000, depending on how complex your application is.

There are also ongoing costs after obtaining your licence, such as audits and any compliance services you may require.

Below, we’ll outline the different application fees for an AFSL as noted by ASIC:

If you aren’t able to apply online, you’ll need to call ASIC on 1300 300 630 and request a pre-application form or download ASIC’s pre-application form (FS05).

Submitting that will allow ASIC to put together a tailored paper application which they can then send you to fill out.

Why do we need to get an AFSL anyway?

Australia has some of the world’s most stringent financial services regulation. Compliance with the requirements under the AFSL is seen as a way to protect consumers against harmful practices of the industry, and to safeguard the overall reputation and integrity of Australia’s financial services sector.

The role of ASIC in regulating the industry has become even more important since the numerous corporate collapses of the 1990s, the Global Financial Crisis of 2008-09 and the final report of the Financial Services Royal Commission in 2019.

If you need any assistance applying for an AFSL, or ensuring your operations are compliant with your AFSL conditions, get in touch with the experts here at 2account and we’d be more than happy to help.